It is common knowledge that large volumes of data are

being constantly generated and a good portion of this can be used to better

understand a potential borrower. This profusion of data has only provided

greater depth and reach to lenders. The emergence of alternative data as a

catalyst in expanding credit delivery and financial inclusion is unmistakable.

It not only expands the scorable population but also deepens the understanding

of their payment behavior.

The popular saying “the only thing that is constant is

change” applies to the way lenders use technology and scoring solutions to

understand the creditworthiness of applicants. Credit Risk Management has come

a long way from the days when banks used one credit score cut off to decision

loan applications. Risk managers now have a plethora of solution options to

craft a credit policy that hits the right balance between risk and reward.

Traditional vs.

Alternative Data Defined

Traditional data typically refers to data that credit

bureaus maintain on their files. This includes data from loan applications,

credit lines, loan repayment history, credit inquiries, and public information

like bankruptcies. Traditional data is FCRA compliant and the acid test is that

it must be verifiable and disputable by the customer.

Industry research has shown that scoring solutions that

use traditional data cannot score a significant section of the population.

According to the Consumer Financial Protection Bureau (CFPB), these ‘credit

invisibles’ number over 45 million people1. It further

points out that although this segment of the population may not have a regular

loan payment track record, they may still be paying their other bills

regularly. And for this reason, it is very important to track this payment

history – e.g. utility payments – to estimate their credit risk.

Definitions of alternative data may vary, depending on

where you look. But in a broad sense, it pertains to data that includes, but is

not limited to rent payments, mobile phone payments, cable TV payments as well

as bank account information, such as deposits, withdrawals or transfers.

The Pros and Cons of

Alternative Data

While alternative data has a very important role in

financial inclusion, it also has other important benefits. In addition to

improving the assessment of the risk of the customer, it can provide timely

information to lenders on activities that may not be reflected on bureau data.

Further, it enables lenders to provide enhanced customer experience. For

example, when they share an online bank account, the loan application

processing may be faster.

Like traditional data, alternative data is susceptible to

inaccuracies. Consumers may not be able to readily review and correct

alternative data although the standards governing it are constantly changing

and evolving to meet customer and regulatory expectations.

1 Kreiswirth, Brian. “Using alternative

data to evaluate creditworthiness.” 2017. //www.consumerfinance.gov/about-us/blog/using-alternative-data-evaluate-creditworthiness/

I had the opportunity

to participate in the #Lend360 event in Dallas, Texas (Sep 25 – 27 2019)

as a speaker. It was a great event that focused on online lending

industry, especially Fintechs, with over 800 lending professionals and

sponsors in attendance.

I was a member of the panel on “Serving Everyday America: Products and Services for the Non-Prime Market”. I spoke on how #Alternativecreditdata enables lenders to understand and reach their customers in three big ways.

Alternative

Credit Data is now being used by prime as well as non-prime lenders to

book new customers. By using a host of new generation Fair Credit

Reporting Act (FCRA) approved credit risk solutions, lenders can now

understand their customers better and hence tailor products and services

accordingly. Alternative data is also a key component that can help

expand #Financialinclusion initiatives to deliver financial services to

the hitherto unserved sections of society.

In my discussions I highlighted the following three -

1. The

US has an estimated 53 million adults who are outside the purview of

traditional credit bureaus. It is now well known that alternative data

can identify and score approximately 90% of this population

2. Secondly,

alternative data enables lenders to differentiate between consumers

with similar traditional credit bureau profiles. This is because it can

provide granular segmentation and a 360 degee view of applicants that is

possible only when we use FCRA compliant not-tradeline data.

3. Thirdly,

from an acquisition perspective, whatever segments the lender targets

using alternative data, for the same risk – or charge offs – alternative

data is capable of booking more accounts.

In his second term in office, Prime Minister Modi has talked about making

India a US$ 5 trillion economy by 2024-20251. This has not only generated a lot of

debate in India and but also has focused world attention on the Indian economy.

Many may think that

this might be a tall order for a country that till recently was home to the largest

number of utterly poor in the world. But the truth is that India may be closer

to this target than we may realize.

While

all sectors of the economy have to grow rapidly, the financial services sector

has a key role to play to reach the mark. By stepping up its inclusive program

that provides equal access to loans and other financial services to all sections

of society, it can create a multiplier effect.

The

obvious link here is that when a larger number of people borrow, especially the

poor, increased economic activity follows leading to growth in sustainable

means of income for broader sections of society. This, then helps rupture the

“vicious cycle” of poverty.

Public policy planners, to their

credit, have long been aware of the direct relationship between financial

inclusion and swift economic growth. In fact, in 2005, Dr. YV Reddy, the then Governor

of the Reserve Bank of India (RBI) had talked about financial inclusion in his

annual policy statement2. In 2008, the Dr. Rangarajan

Committee on financial inclusion3 recommended

a national mission to facilitate required policy changes.

Despite

all this, India’s progress had obviously been slow in the past. But the economic

fortunes of the poor have changed for the better – quickly and noticeably – only

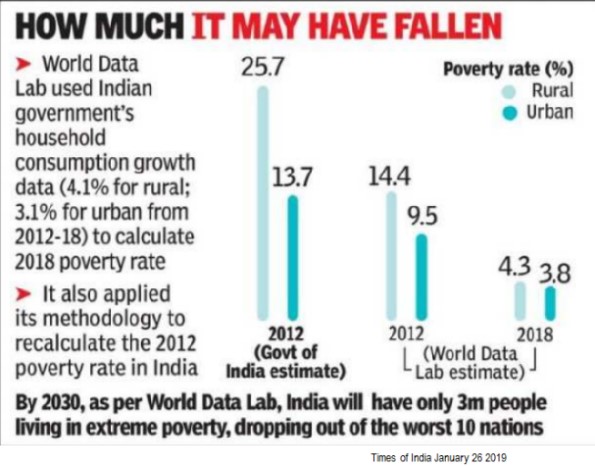

in the last decade. A report published in the Times of India (TOI) in January

2019 quoting World Data Lab showed the steep fall in poverty in India and

estimated the current ‘extreme poor’ to be around 50 million.4 [According

to the World Bank, ‘extreme poor’ are those who make less than $1.9 per

day.]

It is important to see

the declining poverty levels in the context of the massive digital revolution that

is taking place in India in parallel. Contrary to what the electronic and print

media in India may have you believe, the digital revolution on multiple fronts

has aided and catalyzed the financial inclusion programs of the government.

As of December 2018, 1.23 billion people had Aadhar digital biometric

identity cards5 and over 1.21 billion

had mobile phones.6 Also, as of 2017, 80% of adults had a

bank account .7 Bulk of the new accounts were opened

with the aid of Aadhar identity cards.

Further, the country has also seen steep rise

in mobile payment transactions. According to the data released by

the National Payments Corporation of India (NPCI)

8 transactions via the Unified Payments Interface

(UPI), the country’s flagship payments platform, grew 25% and crossed Rs.1

trillion in value in December 2018.

However, millions

continue to live in poverty. India has a low credit access with only 154 loans

per 1000 adults7. This may be attributed to the

reluctance of lenders to lend to people whose credit worthiness cannot be

reasonably assessed. Unlike the US, India does not have robust credit reporting

agencies with depth of data that can help lenders in approving loans. This remains

a major challenge for credit expansion.

The good news, however,

is that the confluence of mobile penetration, establishment of a biometric

identity and the emergence of disruptive credit risk solutions that facilitate

the identification and assessment of borrower risk may set the scene for

massive credit inclusion process. Consequently, India’s efforts to eliminate

poverty may have reached a tipping point.

Many fintechs around

the world and in India are now using a consumer’s digital identity to predict

loan repayment behavior. In a report published in September 2018, the Federal

Deposit Insurance Corporation (FDIC) of the US has reported9 that

a predictive “model that uses only the digital footprint variables equals or exceeds

the information content of the credit bureau score”.

In other words, lenders

in India will now be able to assess credit risk of borrowers by using their

digital identity. This also simultaneously obviates the need to build credit

bureaus using traditional data – an expensive and time consuming effort in any

case.

The purpose of this

piece is not to speculate if India will reach the US$ 5 trillion mark by

2024-25, but to rather assess its preparedness in setting in motion a host of

services and programs that will benefit the largest number of poor. As is obvious, lifting millions of people out

of poverty is a multi-pronged, multi-mission driven exercise where the happy

meeting of cutting-edge technology and robust political will to execute the

mission are necessary and imperative conditions.

India has adequately

demonstrated its capability to execute complex projects on time and within

budget. This augers well for the extreme poor. If they rise up above poverty, so

will India, economically speaking, and crossing the US$ 5 trillion mark may

just be one of the milestones.

Modi’s achievements in

this regard, as substantiated by data from multiple sources, are substantial

and suggest that it is broad-based and truly inclusive. This is in stark

contrast to the efforts of the earlier government led by Dr Manmohan Singh who

claimed at the National Development Council that “the first claim on the

country’s resources for development”10were reserved exclusively for a particular religious

community.

It is indeed debatable if India, in its tryst with destiny, ever

managed to redeem its pledge, as Pandit Jawaharlal Nehru dreamt at that

midnight hour in 1947. Definitely data suggests that even after almost

six decades, the redemption of the pledge in terms of poverty

eradication, was not even substantial. But given the track record of

the last five years, Modi’s tryst with India is taking it places and the

poorest of poor are joining the bandwagon in their millions. And Modi

has the backing of the state-of-art technology. Of course, the claim on

the country’s resources for development will be inclusive and for all,

not the exclusive right of a select few.

The emergence of

alternative data as a key enabler in expanding credit delivery and financial

inclusion is unmistakable.

The

saying that the only thing that is constant is change, is attributed to

Heraclitus, the Greek Philosopher. This is so very relevant today in the way

lenders use technology and scoring solutions to understand the credit

worthiness of applicants. Credit Risk Management has come a long way from the

days when banks used just one credit score cut off to decision loan

applications. Risk managers now have a plethora of solution options to enable

them to craft the right risk reward balance when they design a credit policy

that would suit them.

It

is common knowledge that large volumes of data are being constantly generated

and a good portion of this can be used to better understand a potential

borrower. This profusion of data has only provided greater depth and reach to

lenders.

The emergence of alternative data as a key enabler

in expanding credit delivery and financial inclusion is unmistakable. It not

only expands the scorable population, but also deepens the understanding of

their payment behavior. The three credit bureaus, realizing the value of this

data asset have embarked on an acquisition spree.

A

basic definition of traditional data as well as alternative data will help

understand the scenario better.

Traditional Data

Traditional

data typically refers to data that credit bureaus maintain on their files. This

includes data provided by the customer in the loan applications, data on credit

lines, loan repayment history, credit enquiries as well as public information

like bankruptcies. Traditional data is FCRA compliant and the acid test is that

it must be verifiable and disputable by the customer.

Industry

research has shown that scoring solutions that use traditional data cannot

score a significant section of the population. According to the Consumer

Financial Protection Bureau (CFPB), these ‘credit invisibles’ number over 45

million people. It further points out that although this segment of the

population may not have a regular loan payment track record, they may still be

paying their other bills regularly. It is thus very important to track this

payment history – e.g. utility payments – to estimate their credit risk.

Alternative Data

Definitions

of alternative data may vary, depending on where you choose to look them up.

But in a broad sense it pertains to data that includes, but limited to rent payments,

mobile phone payments, Cable TV payments as well as bank account

information, such as deposits, withdrawals or transfers.

While

alternative data has a very important role in financial inclusion, it also has

other important benefits. In addition to improving the assessment of the risk

of the customer, it can provide timely information to lenders on activities

that may not be reflected on bureau data. Further it enables lenders to provide

enhanced customer experience. For example, when they share online bank account,

the loan application processing may be faster.

Like

traditional data, alternative data to is susceptible to inaccuracies. Consumers

may not be able to readily review and correct alternative data although the

standards governing it are constantly changing and evolving to meet customer

and regulatory expectations.