In his second term in office, Prime Minister Modi has talked about making

India a US$ 5 trillion economy by 2024-20251. This has not only generated a lot of

debate in India and but also has focused world attention on the Indian economy.

Many may think that

this might be a tall order for a country that till recently was home to the largest

number of utterly poor in the world. But the truth is that India may be closer

to this target than we may realize.

While

all sectors of the economy have to grow rapidly, the financial services sector

has a key role to play to reach the mark. By stepping up its inclusive program

that provides equal access to loans and other financial services to all sections

of society, it can create a multiplier effect.

The

obvious link here is that when a larger number of people borrow, especially the

poor, increased economic activity follows leading to growth in sustainable

means of income for broader sections of society. This, then helps rupture the

“vicious cycle” of poverty.

Public policy planners, to their

credit, have long been aware of the direct relationship between financial

inclusion and swift economic growth. In fact, in 2005, Dr. YV Reddy, the then Governor

of the Reserve Bank of India (RBI) had talked about financial inclusion in his

annual policy statement2. In 2008, the Dr. Rangarajan

Committee on financial inclusion3 recommended

a national mission to facilitate required policy changes.

Despite

all this, India’s progress had obviously been slow in the past. But the economic

fortunes of the poor have changed for the better – quickly and noticeably – only

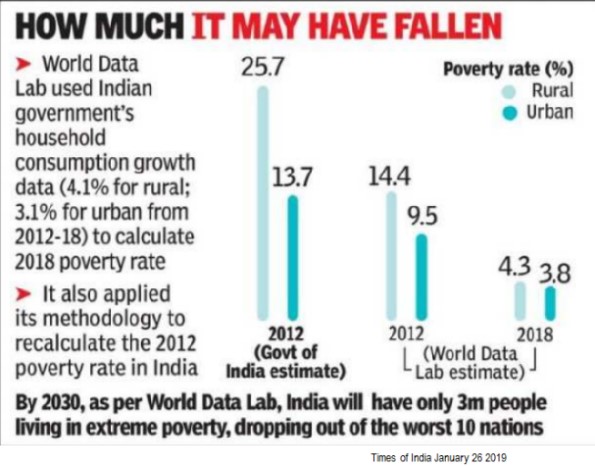

in the last decade. A report published in the Times of India (TOI) in January

2019 quoting World Data Lab showed the steep fall in poverty in India and

estimated the current ‘extreme poor’ to be around 50 million.4 [According

to the World Bank, ‘extreme poor’ are those who make less than $1.9 per

day.]

It is important to see

the declining poverty levels in the context of the massive digital revolution that

is taking place in India in parallel. Contrary to what the electronic and print

media in India may have you believe, the digital revolution on multiple fronts

has aided and catalyzed the financial inclusion programs of the government.

As of December 2018, 1.23 billion people had Aadhar digital biometric

identity cards5 and over 1.21 billion

had mobile phones.6 Also, as of 2017, 80% of adults had a

bank account .7 Bulk of the new accounts were opened

with the aid of Aadhar identity cards.

Further, the country has also seen steep rise

in mobile payment transactions. According to the data released by

the National Payments Corporation of India (NPCI)

8 transactions via the Unified Payments Interface

(UPI), the country’s flagship payments platform, grew 25% and crossed Rs.1

trillion in value in December 2018.

However, millions

continue to live in poverty. India has a low credit access with only 154 loans

per 1000 adults7. This may be attributed to the

reluctance of lenders to lend to people whose credit worthiness cannot be

reasonably assessed. Unlike the US, India does not have robust credit reporting

agencies with depth of data that can help lenders in approving loans. This remains

a major challenge for credit expansion.

The good news, however,

is that the confluence of mobile penetration, establishment of a biometric

identity and the emergence of disruptive credit risk solutions that facilitate

the identification and assessment of borrower risk may set the scene for

massive credit inclusion process. Consequently, India’s efforts to eliminate

poverty may have reached a tipping point.

Many fintechs around

the world and in India are now using a consumer’s digital identity to predict

loan repayment behavior. In a report published in September 2018, the Federal

Deposit Insurance Corporation (FDIC) of the US has reported9 that

a predictive “model that uses only the digital footprint variables equals or exceeds

the information content of the credit bureau score”.

In other words, lenders

in India will now be able to assess credit risk of borrowers by using their

digital identity. This also simultaneously obviates the need to build credit

bureaus using traditional data – an expensive and time consuming effort in any

case.

The purpose of this

piece is not to speculate if India will reach the US$ 5 trillion mark by

2024-25, but to rather assess its preparedness in setting in motion a host of

services and programs that will benefit the largest number of poor. As is obvious, lifting millions of people out

of poverty is a multi-pronged, multi-mission driven exercise where the happy

meeting of cutting-edge technology and robust political will to execute the

mission are necessary and imperative conditions.

India has adequately

demonstrated its capability to execute complex projects on time and within

budget. This augers well for the extreme poor. If they rise up above poverty, so

will India, economically speaking, and crossing the US$ 5 trillion mark may

just be one of the milestones.

Modi’s achievements in

this regard, as substantiated by data from multiple sources, are substantial

and suggest that it is broad-based and truly inclusive. This is in stark

contrast to the efforts of the earlier government led by Dr Manmohan Singh who

claimed at the National Development Council that “the first claim on the

country’s resources for development”10were reserved exclusively for a particular religious

community.

It is indeed debatable if India, in its tryst with destiny, ever

managed to redeem its pledge, as Pandit Jawaharlal Nehru dreamt at that

midnight hour in 1947. Definitely data suggests that even after almost

six decades, the redemption of the pledge in terms of poverty

eradication, was not even substantial. But given the track record of

the last five years, Modi’s tryst with India is taking it places and the

poorest of poor are joining the bandwagon in their millions. And Modi

has the backing of the state-of-art technology. Of course, the claim on

the country’s resources for development will be inclusive and for all,

not the exclusive right of a select few.